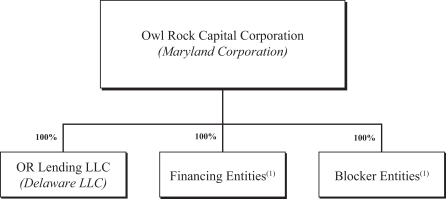

Corporate Structure

On April 27, 2016, we formed a wholly-owned subsidiary, OR Lending LLC, a Delaware limited liability company, which holds a California finance lenders license. OR Lending LLC originates loans to borrowers headquartered in California. From time to time we may form wholly-owned subsidiaries to facilitate our normal course of business.

Our portfolio is subject to diversification and other requirements because we have elected to be regulated as a BDC under the 1940 Act and as a RIC for U.S. federal income tax purposes. We made our BDC election on March 3, 2016. We intend to maintain these elections. See “Regulation” for more information on these requirements.

The following chart depicts our ownership structure:

| (1) | From time to time the Company may form wholly-owned subsidiaries to facilitate the normal course of business. |

The Adviser — Owl Rock Capital Advisors LLC

The Adviser serves as our investment adviser pursuant to an investment advisory agreement between us and the Adviser. The Adviser is registered with the SEC as an investment adviser under the U.S. Investment Advisers Act of 1940, as amended (the “Advisers Act”). The Adviser is an indirect subsidiary of Owl Rock Capital Partners LP (“Owl Rock Capital Partners”). Owl Rock Capital Partners is led by its three co-founders, Douglas I. Ostrover, Marc S. Lipschultz and Craig W. Packer. The Adviser’s investment team (the “Investment Team”) is also led by Douglas I. Ostrover, Marc S. Lipschultz and Craig W. Packer and is supported by certain members of the Adviser’s senior executive team and the investment committee (the “Investment Committee”). The Investment Committee is comprised of Douglas I. Ostrover, Marc S. Lipschultz, Craig W. Packer and Alexis Maged. The Adviser has limited operating history. Subject to the overall supervision of the Board, the Adviser manages our day-to-day operations, and provides investment advisory and management services to us.

The Adviser also serves as investment adviser to Owl Rock Capital Corporation II. Owl Rock Capital Corporation II is a corporation formed under the laws of the State of Maryland that, like us, has elected to be treated as a BDC under the 1940 Act. Owl Rock Capital Corporation II’s investment objective is similar to ours, which is to generate current income, and to a lesser extent, capital appreciation by targeting investment opportunities with favorable risk-adjusted returns. As of December 31, 2018, Owl Rock Capital Corporation II had raised gross proceeds of approximately $449.0 million, including seed capital contributed by the Adviser in September 2016 and approximately $10.0 million in gross proceeds raised from certain individuals and entities affiliated with the Adviser.

The Adviser is affiliated with Owl Rock Technology Advisors LLC (“ORTA”) and Owl Rock Capital Private Fund Advisors LLC (“ORCPFA”), which also are investment advisers and subsidiaries of Owl Rock

3